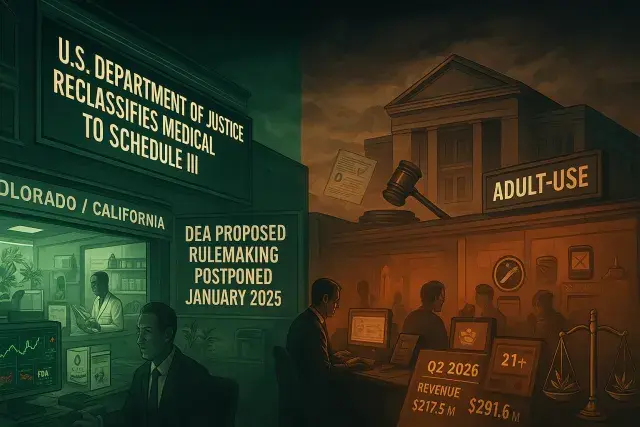

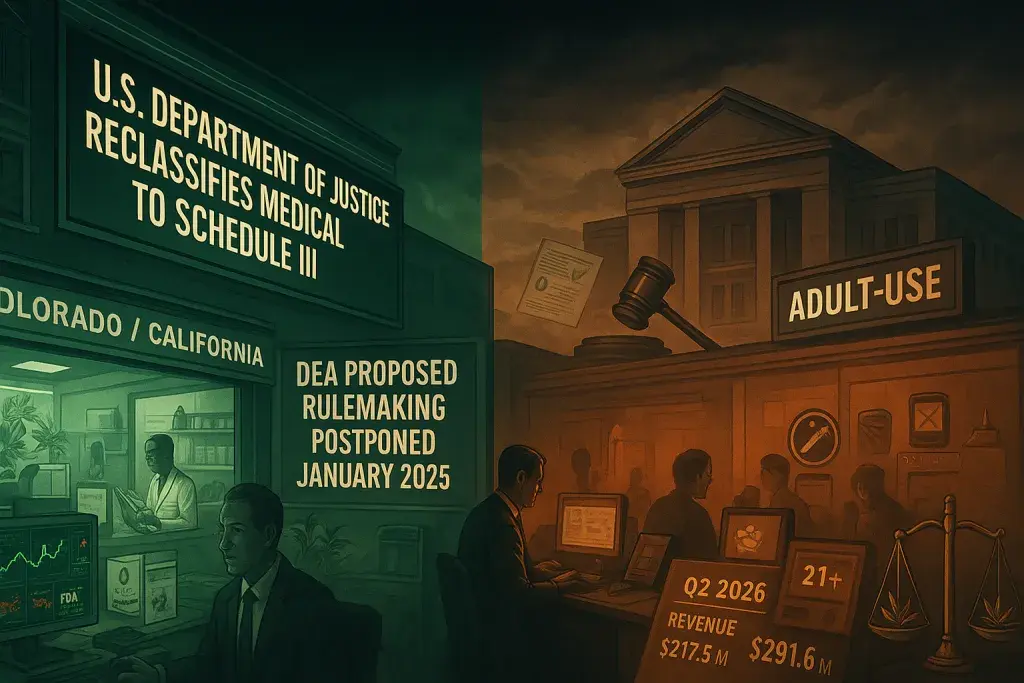

Tilray Brands surged in premarket trading after the U.S. Department of Justice announced it would reclassify FDA-approved and state-licensed medical cannabis products to Schedule III - then reversed much of that move as investors worked through what the action actually covers. The pattern was familiar: a policy headline runs ahead of the policy itself, and the market spends the rest of the session catching up. For operators and investors trying to read federal signals, that gap between headline and substance is where the real work happens.

The rally reflected genuine excitement about a federal posture shift that the industry has been waiting on for years. But the reclassification applies to medical cannabis operating under FDA approval and state licensing - not to the adult-use market that drives the majority of dispensary revenue across states from Colorado to California. That distinction matters enormously for licensed operators thinking about their compliance obligations, tax treatment, and banking relationships. Retailers running point-of-sale systems in more regulated state markets - operators familiar with tools like cannabis pos maine deployments - already know that state licensing structures and federal classification exist in uneasy parallel, and that a federal tweak to the medical side doesn't automatically smooth the adult-use side of the ledger.

It's also worth being precise about where the federal process actually stands. The DEA's proposed rescheduling rulemaking has been active for months. A hearing on the proposal was postponed in January 2025 pending further proceedings. That means the industry isn't dealing with a settled regulatory outcome - it's dealing with an active rulemaking that could still face legal challenges, procedural delays, or revisions. For operators managing compliance calendars, that distinction between a proposed rule and a final rule is not a technicality. It's the difference between planning around something real and speculating on something contingent.

What Schedule III Actually Changes - and What It Doesn't

The core question for any cannabis business is commercial: does this reclassification change what you can do, what you owe, or how you operate? On the medical side, the answer may eventually be yes. Reuters reported that Schedule III status could improve research access, reduce certain tax burdens, and help medical cannabis operators on margins that have been squeezed by federal tax policy. Specifically, Section 280E of the Internal Revenue Code - which disallows standard business deductions for companies trafficking in Schedule I or Schedule II controlled substances - has been one of the most punishing structural disadvantages facing licensed cannabis businesses. A Schedule III reclassification could change that calculation for medical operators, though legal interpretation will matter and the rulemaking isn't final.

For adult-use dispensaries, none of that changes. The federal conflict around recreational cannabis remains unresolved. Multi-state operators running adult-use retail in states where it's licensed still face the same banking constraints, the same payment friction, and the same 280E exposure they did before the announcement. That's not a small carve-out - adult-use is where most of the commercial volume sits. The rescheduling action as described is a meaningful step for the medical channel. It doesn't restructure the adult-use market's relationship with federal law.

Tilray's Position in a Narrower Opportunity

Here's the thing: Tilray came into this headline with a more defensible medical-cannabis thesis than many of its peers. The company reported record fiscal Q2 2026 net revenue of $217.5 million. International medical cannabis revenue grew 36% in that period. Its Tilray Pharma segment - a pharmaceutical distribution platform management has described as a $300 million opportunity - posted a quarterly revenue record of $85.3 million. The company also reported $291.6 million in cash and marketable securities and reaffirmed fiscal 2026 adjusted EBITDA guidance of $62 million to $72 million.

Management has been explicit about how it sees rescheduling fitting the business: as an opening for medical cannabis research, patient access, and product development in the U.S., anchored by what it calls Tilray Medical U.S. That's a more structured claim than a pure speculation play, and it helps explain why investors were quick to bid the stock when the headline dropped. The platform is real. The question is timing - and timing in cannabis policy has a long track record of disappointing the market's optimism about how quickly things actually move.

The Slow Rulemaking Clock and What Operators Should Watch

For dispensary operators, wholesalers, and cannabis brands trying to make operational decisions, the honest read here is cautious. The federal direction on medical cannabis is more favorable than it was. The rulemaking is still proceeding. The adult-use framework is unchanged. And 280E relief - if it materializes for medical operators - would represent a real improvement in unit economics for those businesses, not a marginal one.

What licensed businesses should actually be tracking is the DEA rulemaking calendar, any legal challenges filed to the proposed rule, and whether Congress moves separately on broader cannabis legislation. Those three threads will determine whether this federal posture shift becomes something operators can build around. In the meantime, the stock's rally and reversal were a clean demonstration of how policy enthusiasm and policy reality continue to move at very different speeds in this industry. The headline moved fast. The rule is still pending.