The SAFE Banking Act has not moved in the 119th Congress - and with Republican leadership controlling both chambers, there is no clear path to a floor vote in the near term. That matters enormously to the licensed cannabis businesses operating right now: dispensary owners negotiating expensive banking relationships, multi-state operators managing payroll in cash, and compliance teams filing currency transaction reports that most retail businesses never think about. The Schedule III reclassification signed in April changed the federal regulatory posture on medical cannabis, but it did not fix the banking problem. Not even close.

Why Schedule III Does Not Solve the Banking Gap

The Trump administration's April 22 order reclassifying state-licensed medical cannabis to Schedule III under the Controlled Substances Act was a meaningful regulatory shift - it acknowledges medicinal value and reduces certain federal restrictions. But here's the catch: financial institutions are not governed by the Controlled Substances Act alone. They operate under the Bank Secrecy Act and federal anti-money laundering statutes, and those frameworks have not changed. A bank that opens a business checking account for a dispensary still faces the same federal exposure it did before reclassification. The legal risk calculus for a compliance officer at a regional bank has not materially improved.

Senator Jeff Merkley, D-Ore., put it plainly: the Schedule III designation still leaves cannabis businesses in violation of criminal law for nonmedical purposes. Adult-use operations - which represent the majority of licensed retail cannabis businesses in most legal states - remain in a federal legal gray zone that no bank's legal team is eager to occupy without explicit statutory protection. That protection is exactly what the SAFE Banking Act was designed to provide, and it does not yet exist.

The Operational Cost of Legislative Inaction

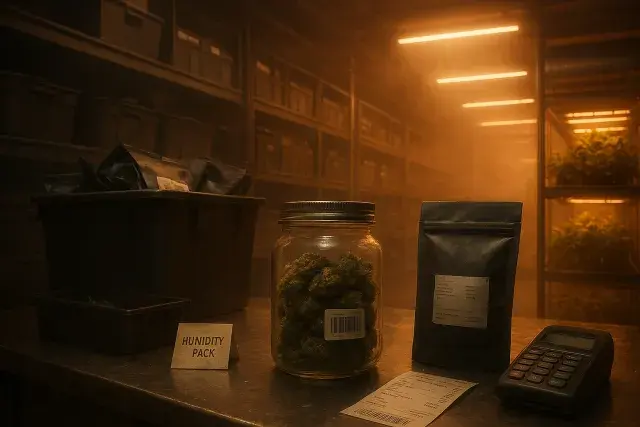

This is not an abstract policy debate. The daily mechanics of running a dispensary without reliable banking access are punishing. Cash-intensive operations require armored transport, on-site safes, elaborate reconciliation processes, and compliance documentation that most retailers never touch. POS systems at cannabis dispensaries often run parallel cash-management workflows specifically because card processing remains inconsistent or structured through workaround payment rails - some of which have drawn regulatory scrutiny of their own. Every workaround carries cost and risk.

The financial institutions that do serve cannabis businesses - primarily regional banks and a small share of credit unions - typically charge a premium to offset their compliance burden. Filing Suspicious Activity Reports on cannabis clients is a standard requirement under current federal guidance, even for fully licensed, state-compliant operators. That compliance overhead gets passed back to dispensary operators in the form of higher account fees. A 2023 Reuters report estimated that roughly 10% of banks and 5% of credit unions nationally extend services to the cannabis sector. That figure has not dramatically shifted.

Multiply these frictions across a multi-state operator managing separate banking relationships in each state, reconciling wholesale payments from licensed cultivators and processors, handling payroll for hundreds of retail employees, and trying to maintain audit-ready compliance logs - and the operational drag becomes significant. Larger operators have built internal treasury functions to manage the exposure. Smaller independent dispensaries often have no such infrastructure. The burden falls hardest on the businesses with the fewest resources to carry it.

Where the Legislation Actually Stands

The SAFE Banking Act passed the House seven times between 2019 and 2022 under Democratic leadership, and the Senate Banking Committee advanced it in 2023. That legislative momentum is, for now, largely absent. Senator Steve Daines, R-Mont. - who had been the primary Republican champion for the bill - announced in March that he would not seek re-election, removing the most visible cross-aisle advocate from the picture. His staff have pointed to freshman Senator Bernie Moreno, R-Ohio, as a potential Republican lead on the Banking Committee. In June 2025, Moreno described the bill as "a tomorrow thing" that would follow budget matters. That is not a commitment; it is a deferral.

Senate Banking Committee Chairman Tim Scott, R-S.C., acknowledged the "quandary" the industry faces at the Milken Institute Global Conference - recognizing both the logic of the legislation and the heightened criminal risks that cash-only cannabis operations create. Scott had previously voted against the SAFE Banking Act over concerns about potential money-laundering loopholes. His communications director subsequently indicated it would be inappropriate to speculate on legislation not yet introduced in the current Senate. That is a careful non-answer, and the industry knows it.

Meanwhile, Senate Majority Leader John Thune, R-S.D., has opposed the SAFE Banking Act in prior congresses. If the bill is never brought to the floor, he does not need to actively block it. The architecture of Republican leadership in both chambers creates structural headwinds that have nothing to do with the merits of cannabis banking reform - and everything to do with political priority-setting in a crowded legislative calendar.

Pressure Building From the States

The absence of federal action has not gone unnoticed at the state level. In August 2025, a bipartisan group of 32 attorneys general from 28 states, Washington, D.C., and three U.S. territories formally urged Congress to resolve the conflict between state-licensed cannabis programs and federal banking law. That is a significant signal - attorneys general from red and blue states alike are putting their names on a letter that essentially says: your inaction is creating law enforcement and public safety problems in our jurisdictions.

The public safety argument is not rhetorical. Cash-dependent retail businesses are robbery targets. Employees handling large cash deposits face risk that employees at any other licensed retail operation do not. State regulators and law enforcement in legal cannabis markets have documented this pattern repeatedly. Senator Scott referenced it directly in his Milken remarks. The argument for solving the banking access problem is not just pro-industry; it is a straightforward public safety and anti-crime argument - one that a Republican-led Congress might be expected to find more compelling than it apparently does.

What's striking here is the gap between stated acknowledgment and legislative action. The industry is not asking for legalization. It is asking for access to the same basic financial services that any other licensed retail business takes for granted: a checking account, a payroll processor, a merchant services relationship. The fact that this remains unresolved - after years of bipartisan floor votes, after reclassification, after dozens of attorneys general put it in writing - says something about where cannabis sits in the federal legislative queue. For operators on the ground, that queue is an expensive place to wait.